Managing a community bank’s balance sheet is like taking care of a home: it requires ongoing maintenance, thoughtful planning, and proactive decisions to preserve its value and ensure long term sustainability. Just as a well-maintained house stands strong through storms and shifting seasons, a carefully tended bond portfolio anchors a community bank’s balance sheet against economic turbulence. For community banks, certain bonds are more than just a safe haven; they’re a critical tool for stabilizing income, managing risk, and preserving margins. Today, with the 5-year Treasury yield hovering at its highest average level in 17 years, banks have a unique opportunity to “renovate” their portfolios, ensuring resilience for years to come.

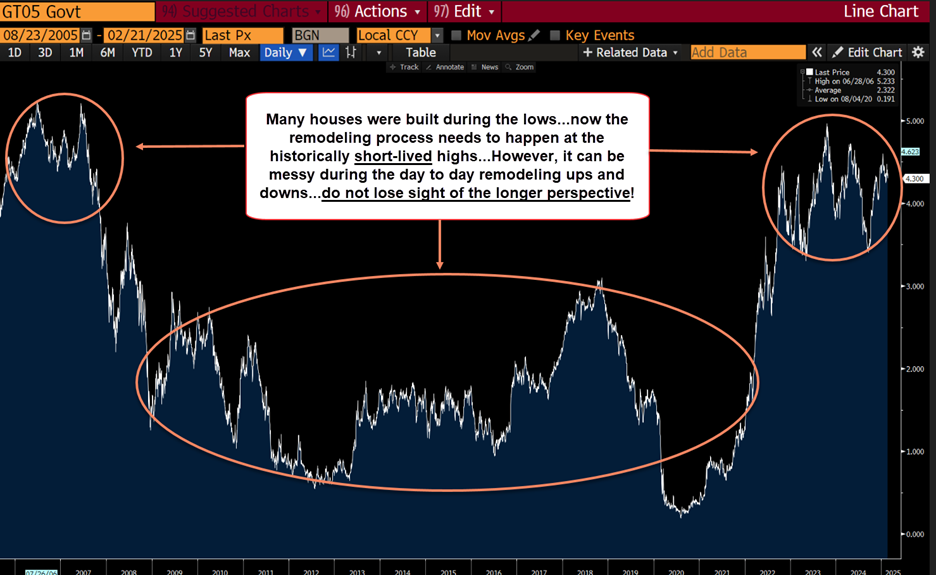

Think of a bond portfolio as the foundation of a house. Neglect it, and cracks appear—margins erode, and vulnerabilities emerge. Maintain it, and it provides steady support. Right now, the 5-year Treasury yield offers a golden window for reinforcement. This part of the yield curve is often viewed as a good proxy for bank portfolios, considering their average lives tend to be around 5 years. As of February 24, 2025, this yield has averaged around 4.20% over the past year, a peak not seen consistently since 2007. Historical data over the last 20 years reveals this moment’s rarity. From 2005 to 2007, yields fluctuated between 4% and 5%, but the post-financial crisis era slashed them to historic lows, averaging below 2% from 2011 to 2021. This is not suggesting yields are going to drop in similar dramatic fashion, however, as risk managers we must anticipate such an occurrence. Today’s rates signal a return to robust performance—a chance to remodel the portfolio before rates potentially decline again.

Am I suggesting we prioritize bonds over loans? Certainly not! At community banks, loans will be and should be the primary vehicles used to serve the local economy, businesses, and households. However, when loan demand is strong there is a tendency to ignore the bond portfolio. During these times, loans can be like the exciting new addition to your house—lucrative when times are good, but prone to leaks (refinancing or defaults) when rates drop or the economy falters. In low-rate environments, borrowers refinance at lower costs, shrinking bank margins, or worse, default during downturns, leaving banks exposed. Bonds, especially those with predictable cash flows and structure, offer a stable yield vehicle to complement the loan portfolio. Selective bonds with specified collateral tend to not refinance unpredictably or default; they pay reliably, providing a buffer against loan volatility. This stability is a lifeline for community banks aiming to protect their net interest margins.

To seize this opportunity, banks should adopt or simply maintain a dollar-cost averaging strategy—steadily investing in these elevated yields over time. Just as you wouldn’t renovate your entire house in one frantic weekend, don’t chase the market in a single leap. By spreading purchases across months, banks lock in today’s high yields, building a portfolio that thrives even if rates fall. Make no mistake, market yield volatility is a daily reality we’re currently experiencing with political climate changes and global economic uncertainty. So, during this time, remember that remodeling is messy from day to day and stay focused on the long-term benefits. Consider this, a 4.5% yield today could be the cushion our margins need if future yield environments are significantly lower, as they have been in past cycles.

Call to Action: Find ways to participate and don’t miss this market opportunity

The graph above underscores the urgency—yields haven’t been this high since before the Great Recession. Missing this market is like letting your house decay until the roof caves in. Community banks must act now, reinforcing their bond portfolios to weather future storms. With market yields at almost two decades high on average, this isn’t just maintenance—it’s a strategic upgrade. Don’t wait for the next downturn to regret a crumbling foundation. Invest now, dollar by dollar, and build a balance sheet that stands firm.

John D. Bloss is a managing partner and serves on the board of directors for The Baker Group. He works primarily with banks in the areas of investments and asset/liability management. He also assists clients in a broad range of other sectors including education, portfolio management evaluation, interest rate risk, strategic planning, and regulatory issues. John focuses on identifying the specific objectives of the clients he serves and tailors investment portfolios to achieve their goals. In that process, he evaluates the relative values of a broad range of investment products and helps clients select those that complement their investment portfolio and overall balance sheet.